Smerdoff / AI for Insurance Agencies

AI Adoption for Insurance Agencies

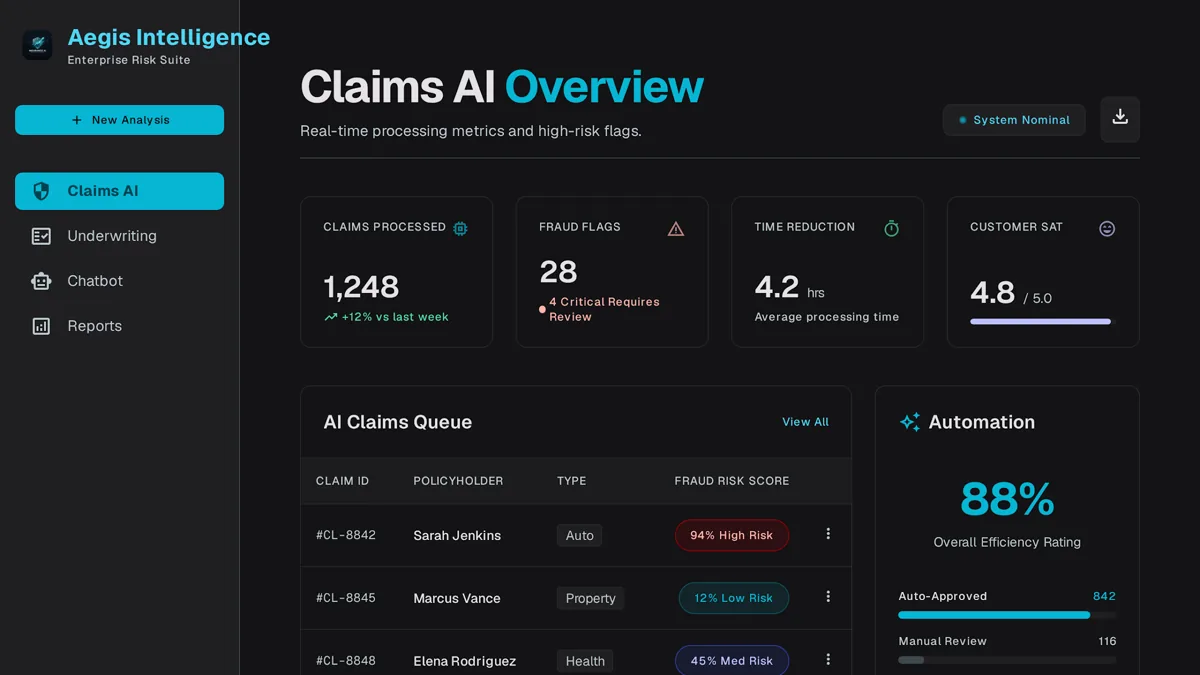

Most claims and underwriting AI is built for carriers running enterprise-scale platforms. We build focused AI features — claims triage with fraud scoring or underwriting automation — sized and priced for an independent agency.

Claims TriageFraud Risk ScoringUnderwriting AutomationFaster Turnaround